Creating a Family Budget: Step-by-Step Guide

Establishing a family budget is essential for managing household finances effectively. A well-structured budget helps families allocate their income towards necessary expenses, savings, and discretionary spending, ensuring that financial goals are met.

To create a family budget, start by listing all sources of income and fixed expenses, such as rent or mortgage, utilities, and groceries. Next, identify variable expenses and discretionary spending categories. By tracking spending over a month, families can adjust their budget to reflect realistic financial habits and goals, ultimately leading to better financial stability.

Advanced Budgeting Techniques for Financial Growth

Once a basic budget is established, families can explore advanced budgeting techniques that promote financial growth. These methods include zero-based budgeting, the envelope system, and the 50/30/20 rule, which help individuals prioritize spending and increase savings.

For example, zero-based budgeting requires every dollar of income to be allocated to specific expenses, savings, or debt repayment, ensuring that no money is left unaccounted for. The envelope system involves using cash for different spending categories, helping to control overspending. Implementing these techniques can lead to a more disciplined approach to finances and improved long-term financial health.

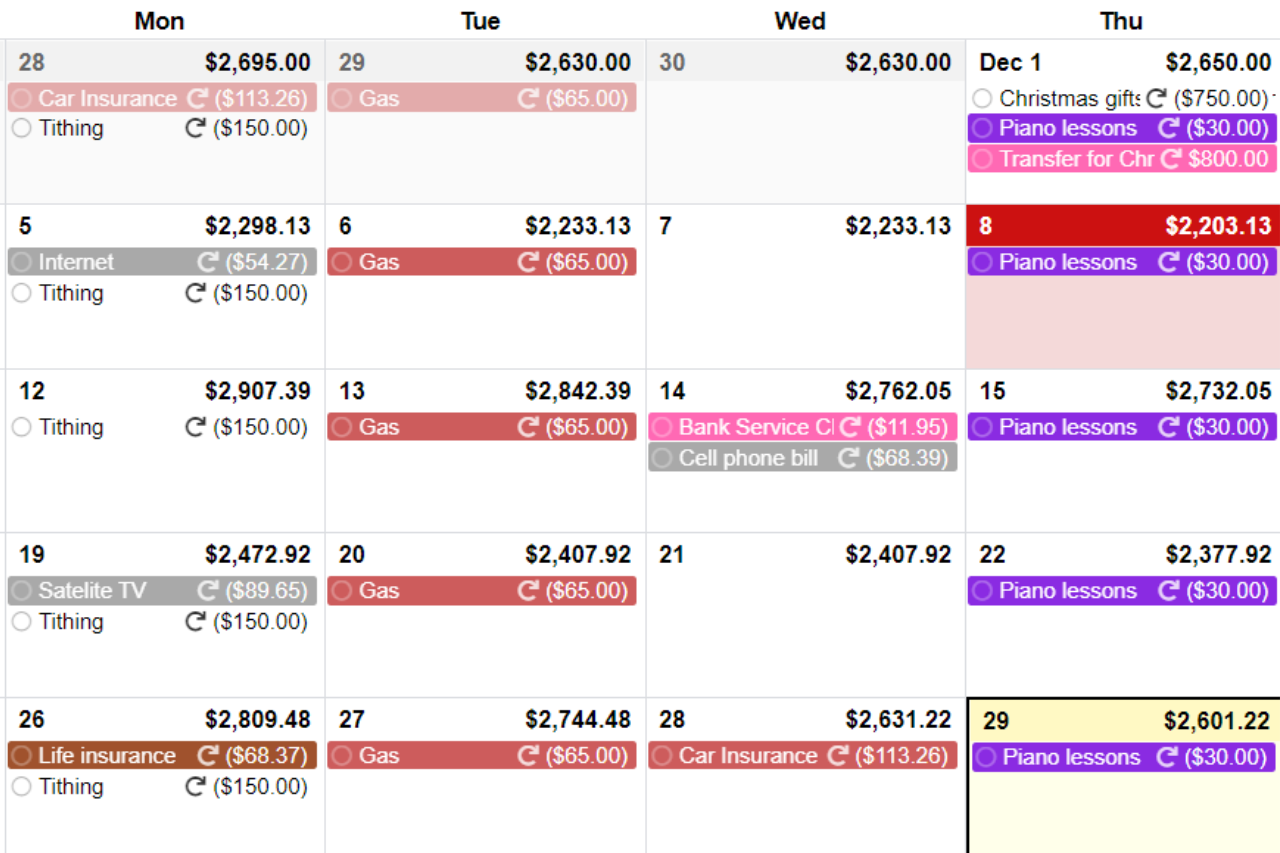

The Role of Technology in Modern Budgeting

Technology plays a significant role in simplifying the budgeting process for families. With the rise of budgeting apps and financial management software, users can easily track expenses, set financial goals, and analyze spending patterns in real-time.

For instance, CalendarBudget offers features that allow users to visualize their financial data, making it easier to identify trends and adjust spending habits accordingly. These tools often come with budgeting templates, reminders, and alerts that help users stay on track, ensuring they adhere to their financial plans and make informed decisions.

Building an Emergency Fund: Why It Matters

Establishing an emergency fund is a crucial aspect of financial planning. This fund acts as a safety net for unexpected expenses, such as medical emergencies or car repairs, preventing families from falling into debt when unforeseen circumstances arise.

Financial experts recommend saving three to six months' worth of living expenses in an easily accessible account. By prioritizing the creation of an emergency fund within their budget, families can achieve greater peace of mind and financial security, allowing them to focus on long-term financial goals without the constant worry of unexpected costs.