Why Should You Pay for Their Mistake? How to Dispute Credit Card Charges and Fight Unfair Billing Errors

Facing an unfair charge can feel overwhelming—especially when it threatens your budget. Knowing your rights and following a clear, practical process makes it much easier to challenge billing errors and get results. This guide breaks down how disputes work, the protections that back you up, and the steps that commonly lead to a fair outcome. If you learn how to spot problems early and act decisively, you can protect your money and reduce stress. Below we cover how to dispute a charge, the consumer rights that matter, strategies for success, and when to escalate or get legal help.

Steps to Dispute a Charge

Disputing a charge is usually a step-by-step process. Staying organized and calm helps you move the issue forward. Typical steps include:

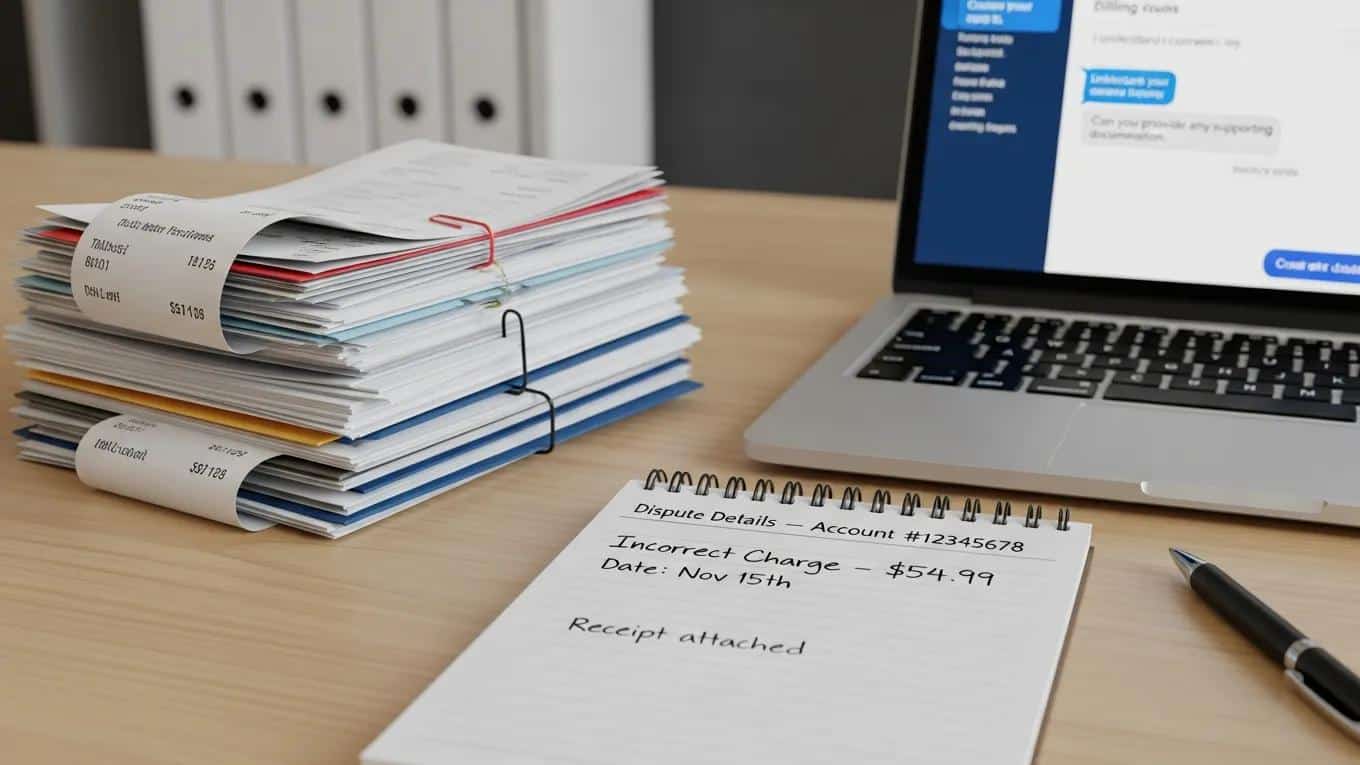

- Gather Documentation: Pull together receipts, billing statements, screenshots, and any messages or emails tied to the charge.

- Contact Customer Service: Call or message the card issuer or merchant to explain the problem and ask for correction.

- Submit a Formal Complaint: If the initial contact doesn’t fix it, follow up with a written dispute that clearly states the charge, the reason it’s wrong, and the supporting evidence.

Using tools like CalendarBudget makes spotting discrepancies easier—tracking your expenses in one place helps you find and act on errors faster.

Relevant Consumer Rights

When you dispute a charge, you’re backed by specific consumer rights. Know these basics so you can push for fair treatment:

- Right to Dispute Charges: You can challenge charges you believe are wrong or unauthorized.

- Right to Request Refunds: If a charge is found to be incorrect, you can ask for your money back.

- Protection from Retaliation: Companies can’t legally punish you for exercising your dispute rights.

These protections come from consumer protection laws designed to keep financial transactions fair and transparent.

Strategies for Successful Resolution

To improve your chances of a favorable outcome, try these practical strategies:

- Educate Yourself: Learn the dispute rules that apply to your card and situation so you know what to expect.

- Utilize Consumer Protection Agencies: If the issuer or merchant won’t cooperate, agencies can help mediate or advise next steps.

- Document Everything: Keep a clear record of dates, names, messages, and evidence—this trail is often decisive.

Applying these tactics makes it easier to reach a timely resolution and shows you’re serious about your claim.

Understanding how dispute agencies operate can also help you decide whether to pursue a non-litigation route or escalate.

Consumer Dispute Resolution & Protection Agencies

Under Law No. 8 of 1999 on Consumer Protection, the Consumer Dispute Resolution Agency serves as a non‑litigation forum for resolving consumer complaints. This study examines that agency’s authority to handle breach-of-performance disputes and considers the impact of Supreme Court Decision No. 275 K/Pdt.Sus-BPSK/2024 on consumer protection.

THE ROLE OF THE CONSUMER DISPUTE RESOLUTION AGENCY IN BREACH OF PERFORMANCE DISPUTES UNDER THE CONSUMER PROTECTION LAW, MRS Putra, 2025

When to Escalate or Seek Legal Assistance

Some disputes can be resolved directly; others need escalation. Consider moving up the chain when:

- Unresolved Issues: Repeated attempts don’t fix the charge.

- Lack of Communication: The company ignores you or gives vague updates.

- Inadequate Compensation: The offer doesn’t fully address your loss or inconvenience.

Escalating at the right time can save you time and preserve your rights—know when to involve regulators or an attorney.

What Are Common Billing Errors and Unfair Charges to Watch For?

Billing mistakes come in many forms. Watch for these common problems:

- Overcharges: You’re billed more than the agreed price.

- Duplicate Charges: The same transaction posts multiple times.

- Incorrect Service Charges: You’re billed for goods or services you didn’t receive.

Spotting these early makes disputing them straightforward.

How Do Billing Errors Occur and What Types Should Consumers Know?

Errors often happen because of simple human or system problems. Typical causes include:

- Data Entry Mistakes: Typos or wrong amounts entered at checkout.

- System Glitches: Software or processing errors that post incorrect charges.

- Miscommunication: Confusion about services or terms between you and the provider.

Knowing how mistakes happen helps you review statements more effectively.

Which Unfair Bank Fees and Unauthorized Charges Are Most Frequent?

Banks and cards sometimes assess fees or charges that feel unfair. Frequently seen examples:

- Unauthorized Charges: Transactions you didn’t approve, often from fraud or identity theft.

- Overdraft Fees: Charges when an account goes negative—sometimes applied even if you quickly cover the balance.

- Monthly Maintenance Fees: Recurring charges for account upkeep that may not have been clearly disclosed.

Knowing these common problems makes it easier to spot and dispute them.

What Consumer Rights Protect You Against Billing Mistakes?

Several safeguards exist to protect consumers from unfair billing. Key protections include:

- Federal and State Laws: Regulations give you the right to dispute charges and seek remedies.

- Consumer Protection Agencies: These organizations can advise, mediate, or take action on your behalf.

- Rights to Dispute Charges: You’re entitled to challenge errors and expect a timely investigation.

These rights give you the tools to push back when billing goes wrong.

Which Laws and Regulations Safeguard Consumers from Unfair Charges?

Several laws help protect you from incorrect or unfair billing, including:

- Fair Credit Billing Act (FCBA): Lets you dispute billing errors on credit card accounts and requires issuers to investigate.

- Truth in Lending Act (TILA): Requires clear disclosure of credit terms so you understand fees and costs up front.

- State Consumer Protection Laws: Many states add extra protections beyond the federal baseline.

Knowing these laws strengthens your position when you file a dispute. Other protections, like the Fair Credit Reporting Act (FCRA), help when false credit information or identity theft is involved.

FCRA & False Credit History Disputes

When an imposter creates false credit history, affected consumers can claim violations of the Fair Credit Reporting Act (FCRA) and related harms—such as invasion of privacy or deceptive trade practices—if agencies fail to correct the record.

Credit Card Litigation, 2001

How Long Do You Have to Dispute a Billing Error or Unauthorized Charge?

Timing matters. Typical limits include:

- 60 Days: Many credit card issuers require disputes to be filed within 60 days of the statement date.

- State-Specific Timeframes: Some states set different deadlines, which can extend or shorten the window.

Check your statements and act quickly to preserve your rights.

How Can You Effectively Dispute Credit Card Charges and Correct Billing Errors?

An effective dispute follows a clear checklist. Core steps are:

- Gather Documentation: Collect receipts, statements, and any proof that supports your claim.

- Contact Customer Service: Report the issue to the card issuer and ask for an investigation.

- Submit a Formal Complaint: If needed, file a written dispute that documents your case and attaches evidence.

Following a consistent method helps your dispute move through the system faster.

What Is the Step-by-Step Process to Challenge Unfair Charges?

To challenge a charge, follow this sequence:

- Identify the Charge: Confirm the exact date, amount, and merchant for the disputed item.

- Gather Evidence: Save receipts, emails, and screenshots that support your claim.

- Contact the Merchant or Issuer: Explain the problem and request a correction or refund.

- Submit a Formal Dispute: If informal contact fails, file a written dispute with the issuer and include your documentation.

This orderly approach improves your chances of a swift, favorable resolution.

What Evidence and Documentation Are Needed to Support Your Dispute?

Strong documentation speeds resolution. Typical items to collect:

- Receipts: Proof of purchase and the agreed price.

- Billing Statements: Statements that show the disputed charge and related transactions.

- Correspondence Records: Emails, chat transcripts, or notes from calls with the merchant or issuer.

Having this information ready makes your dispute clearer and more persuasive.

How Does Using CalendarBudget Help Monitor and Prevent Unfair Charges?

CalendarBudget helps you spot problems early so you can act before they become headaches. Key ways it helps:

- Visual Forecasting: See upcoming and past expenses at a glance, which makes odd charges stand out.

- Goal Setting and Tracking: Keep target spending in view so unexpected charges are easier to notice.

- Expense Tracking: Monitor transactions in real time to spot unauthorized activity sooner.

Using these features gives you more control and reduces the time it takes to catch billing errors.

Which Features of CalendarBudget Assist in Detecting Billing Errors Early?

CalendarBudget includes features designed to make anomalies obvious:

- Visual Calendar Interface: See your bills and payments on a calendar so unusual items are easy to spot.

- Expense Tracking: Track spending as it happens to detect unauthorized charges quickly.

- Reminders for Bill Payments: Automated reminders prevent missed payments and late fees.

These tools help you stay proactive about your finances and catch mistakes faster.

How Can Proactive Budgeting Alerts Empower You to Avoid Fraudulent Charges?

Budgeting alerts give you early warnings so you can act fast. Benefits include:

- Proactive Alerts: Notifications about unusual spending patterns can flag possible fraud.

- Expense Tracking: Continuous monitoring helps you spot unauthorized transactions right away.

- Goal Setting: Clear goals keep your usual spending in check so anomalies stand out.

These features strengthen your ability to detect and stop fraud before it spreads.

What Are Best Practices for Reporting Fraudulent Charges and Following Up?

When you suspect fraud, follow these best practices:

- Gather Documentation: Collect statements, receipts, and any evidence of the fraud.

- Contact Customer Service: Report the fraud to your card issuer and the merchant as soon as possible.

- Follow Up in Writing: Document the report in writing so there’s an official record of your claim.

Consistent follow-up and clear records help ensure your report gets the attention it needs.

Knowing how charge reversals work and the merchant’s role in chargebacks helps you set expectations during the process.

Reversing Fraudulent Credit Card Charges

When a fraudulent charge is disputed and reversed, the merchant typically absorbs the transaction cost and faces a chargeback notification—an outcome that underscores why timely dispute reporting is important for both consumers and merchants.

Understanding credit card frauds, 2003

How Do You Report Fraud to Financial Institutions and Consumer Protection Agencies?

Reporting fraud usually follows a clear path. Key steps are:

- Gather Documentation: Save all relevant statements and correspondence.

- Contact Your Bank: Report the fraud to your financial institution and request a dispute investigation.

- Follow Up in Writing: File written reports with your bank and any relevant consumer protection agencies to create an official record.

These steps help ensure your case is logged and investigated properly.

What Timelines and Follow-Up Steps Ensure Your Dispute Is Resolved?

Keep timelines and follow-up organized to move your dispute forward. Key points:

- Typical Timelines: Issuers often respond to disputes within about 30 days, though full resolution can take longer.

- Follow-Up Strategies: Check in regularly, note every contact, and escalate if responses are delayed.

- Documentation: Preserve copies of every email, letter, and call log related to the dispute.

Staying organized and persistent increases the chance your dispute will be resolved fairly and promptly.

Leave A Comment