Why does a “perfect” budget still leave your bank account in the red?

You can build a careful, well-categorized budget and still get surprised by overdrafts. That usually happens because budgeting and cash flow aren’t the same thing — timing, hidden costs, and variable income create gaps most budgets don’t show. Below we’ll unpack why a seemingly perfect plan can still fail, point out common mistakes, and share practical fixes. You’ll also see how tools like CalendarBudget make cash flow visible so you stop guessing and start planning.

Good budgeting isn’t optional — it’s a foundation for steady finances and smarter debt management, and the research backs that up.

Personal Budgeting for Financial Stability & Debt Mitigation

Personal budgeting builds financial discipline and long-term security. This paper reviews the principles, tools, and tactics that make personal budgets work — from clear goals and expense tracking to adapting plans as circumstances change.

MANAGING YOUR PERSONAL BUDGET, 2024

Budgeting feels straightforward until life happens: missed bills, surprise repairs, or paychecks that come at odd times. That confusion leads to stress and costly overdrafts. This guide walks through the main trouble spots — cash flow timing, hidden costs, and variable income — and gives concrete steps to keep your account in the black.

That view is supported by research showing budgeting gives a clear framework for managing income and spending, which helps people stay disciplined and meet goals.

Effective Budgeting & Cash Flow Monitoring for Personal Finance

Research finds that a detailed budget helps people monitor cash flow, cover essentials, and spot spending they can trim. Budgets also make it easier to set short- and long-term goals and to stay financially responsible.

Budgeting and Saving Effectiveness as the Main Pillar of Sustainable Personal Financial Management, T Prakoso, 2024

Why can a carefully planned budget still go negative?

Even careful budgets break down for predictable reasons. Spotting those causes is the first step to preventing unexpected overdrafts and keeping your finances stable.

Which budgeting mistakes most often cause surprise overdrafts?

Some common errors quietly drain accounts. Watch for these:

- Failure to track all expenses: Small subscriptions and irregular charges add up fast when they’re not tracked.

- Ignoring irregular income: If your pay varies, treating your high-earnings months like the norm can leave you exposed in leaner periods.

- Not planning for annual bills: Taxes, insurance, memberships, and other year‑or twice‑a‑year payments can surprise you if they’re not reserved for.

Fixing these gaps makes your budget far more resilient and less likely to produce nasty surprises.

How do hidden costs and irregular expenses derail your budget?

Hidden and irregular costs are the usual suspects behind a “perfect” budget gone wrong. Common troublemakers include:

- Unexpected repairs: A broken appliance or car repair can wipe out a month’s cushion if you’re unprepared.

- Subscription creep: Multiple small monthly charges you forget about can stealthily eat your balance.

- Seasonal costs: Holidays, back-to-school, and seasonal needs spike spending unless you plan ahead.

Counting these items into your plan — even as rough monthly savings buckets — gives a more accurate picture of what your budget can actually cover.

How does cash flow timing affect your bank balance?

Timing is where budgets and real bank balances diverge. Knowing when money actually lands and when bills clear prevents the timing gaps that trigger overdrafts.

Why is cash flow timing critical to avoiding negative balances?

Cash flow timing means matching when income arrives with when expenses are paid. If bills clear before a paycheck does, you can end up overdrawn even when your monthly math looks correct. This mismatch — not the budget itself — is often the root cause of negative balances.

Studies show that weak cash flow management is a main driver of liquidity problems and payment delays.

Preventing Cash Gaps: Effective Cash Flow Management Strategy

Poor cash flow management often causes liquidity shortfalls and missed payments. A clear financial strategy supports steady cash rhythms and reduces reliance on external financing. Good cash flow planning helps stabilize operations and preserve financial health.

Cash flow management strategy, KV Oriekhova, 2022

How can managing variable income and annual bills prevent overdrafts?

Plan for variability and the odd big bill. Practical steps include:

- Create a buffer: Keep a cushion in your account to cover expenses that land before your next paycheck.

- Save for irregular bills: Move a small amount each month into a sinking fund for annual or semi‑annual expenses.

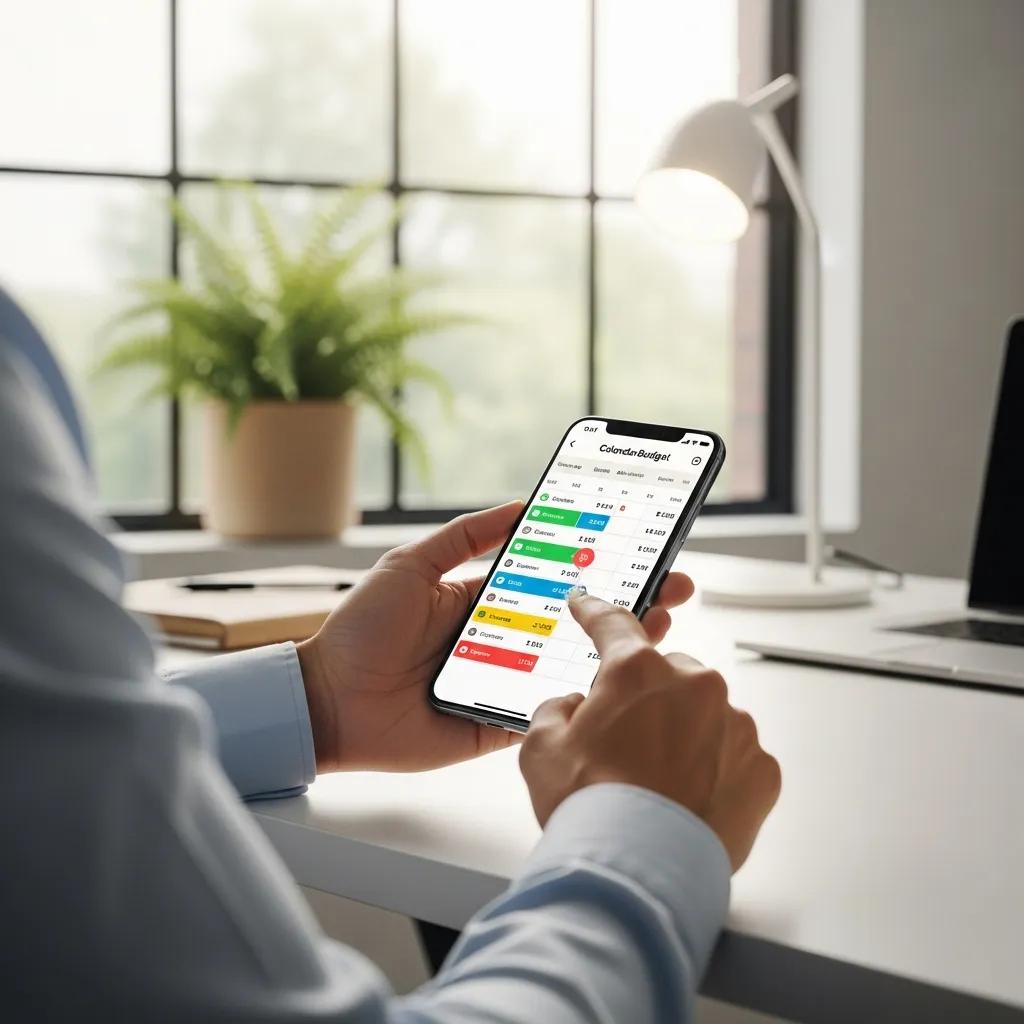

- Use calendar-based tools: Visual tools like CalendarBudget help you map when money comes and goes so you can plan around timing gaps.

Apply these consistently and your cash flow becomes predictable — not stressful.

Which overdraft-prevention strategies keep your account in the black?

Stopping overdrafts is about system and habit. Try these approaches:

- Visual cash flow forecasting: Seeing your balance day by day makes timing problems obvious before they hit.

- Set alerts: Notifications for low balances or upcoming payments give you time to act.

- Review your budget regularly: Weekly or monthly check-ins catch creeping subscriptions, category drift, and one-off expenses early.

How does visual cash flow forecasting improve budget accuracy?

Visual forecasting turns static monthly totals into a timeline you can act on. When you map income and bills across the month, you can spot days when you’ll be thin and move money or shift payments before an overdraft occurs.

What alerts and tools proactively prevent overdraft fees?

Use a mix of bank features and apps to stay in control:

- Banking alerts: Low-balance and upcoming-payment alerts are first-line defenses.

- Budgeting apps: Apps that update in real time help you see how purchases change your future balance.

- Expense trackers: Regular tracking shows where to cut or reallocate dollars before a shortfall.

Combining alerts with a visual plan reduces surprises and keeps fees away.

Key Resources for Daily Budget Tracking & Overdraft Prevention

CalendarBudget was built to make cash flow obvious. By showing your real bank balance day‑by‑day into the future, the app helps you stop guessing and start seeing — so you can move money, shift payments, or delay nonessential spending before a gap becomes an overdraft.

What features in CalendarBudget support better cash flow management?

CalendarBudget includes features designed to keep timing risks visible:

- Visual budgeting: A calendar view that shows when bills and income hit your account.

- Real-time updates: Track spending as it happens so your forecast stays accurate.

- Alerts and notifications: Reminders for upcoming bills and low balances so you can act early.

Those features help you plan around timing issues instead of reacting to them.

Are there real-life examples of users avoiding overdrafts with CalendarBudget?

Yes — many users report avoiding overdrafts after they started planning with a day-by-day view. When people see upcoming shortfalls in the calendar, they move money, pause discretionary spending, or reschedule payments to stay positive.

In short: a technically “perfect” budget can still fail if it ignores timing and irregular costs. By identifying hidden expenses, building buffers, and using visual tools like CalendarBudget, you make your budget real — not just a monthly spreadsheet — and keep your account out of the red.

Leave A Comment