Smart Money Questions to Ask — How the Right Question Can Help You Save

Asking focused financial questions is one of the simplest, most effective ways to take control of your money. Too often people skip the questions that reveal where cash leaks are happening, and that can lead to avoidable spending and stress. This piece shows how asking smarter questions lets you spot waste, tighten your budget, and protect what matters most. We’ll walk through practical questions, look at common spending traps, and show how tools like CalendarBudget make it easier to turn insights into action.

Framing personal finance as a process of curiosity and reflection lines up with teaching methods that emphasize active questioning and critical thinking—skills that help people make better financial choices.

Asking the right question can save you money

I was recently reading an entry in the Thrifty Mommy blog where she knew the right question to ask to get much-needed airline tickets for the next day at a discount price. The entry tells of her savings (others comments on savings they’ve had) by asking for bereavement fares. So she was able to attend to the family loss with the expense being minimized.

Here are some other questions that may help you save on your purchases:

- my parents were doing major house renovations and asked a major hardware store if they would give them a discount because they would need to return often for different supplies needed along the way and some of them would be rather expensive which they did agree to a 15% discount on all purchases

- when you go out to dinner for a birthday/anniversary celebration ask if they would give a discount for the occasion (some regulations may exist – free dessert, must have 3 or 4 other paying adults then you can have the 4th adult meal for free, must be on the person’s birthday with proof of birth date)

- don’t be afraid to ask if there any upcoming sales/discounts in the near future on anything really (food, furniture, car, tires, etc.) or for a rain check on an existing sale when they have run out

- the builder for our house was taking an extremely long time and we gave him a letter telling him kindly that we were not satisfied with the tardiness and some of the quality of the work and wanted to be compensated or would challenge him through the Home Owners Association, which would then give him a fine he’d have to pay. We ended up getting an upgrade of ceramic tiles put into a larger area in our house than the original floor plan said (definitely didn’t cost him as much to have the ceramics installed as he told us originally it would cost us to have it done)

- ask friends if they know of a way to get things at a discount price. A friend of ours knows a car dealer that attends auctions and is able to get cars at a wholesale price and thus possibly able to get a vehicle through them at a discount price

There are numerous other areas you could save on (food, vehicles, art, presentations, vacation/cruise, concerts, etc). You just have to be willing to ask if there is a discount available. Sometimes the savings are huge, other times you have to decide if the effort is worth your time. Really the businesses all want to retain your business and their level of service is usually the only thing that will help them excel above their competition and retain you as a customer (hopefully you will refer your friends as well).

Inquiry-Based Learning for Personal Finance

Inquiry-based learning (IBL) gives students a hands-on way to understand economics by encouraging them to ask questions, investigate, analyze results, and draw conclusions. This approach supports deeper engagement, sharper critical thinking, and better problem-solving—skills especially useful in personal finance. One project described here adapts IBL into a 10-day personal finance unit for a 12th-grade economics course, showing how seniors can use questioning and investigation to learn real-world money skills.

Implementing Inquiry in a High School Economics Course, 2023

What key questions help you spot where money is slipping away?

Finding spending leaks starts with asking the right questions. A few targeted queries can reveal recurring payments, impulse habits, and other drains on your cash flow. Once you know where the holes are, you can plug them—and redirect that money toward savings or priorities.

Which questions surface unnecessary expenses?

Ask yourself these straightforward questions to find expenses you can cut:

- What subscriptions am I paying for? List recurring charges and cancel any services you no longer use or need.

- Am I sticking to my budget? Compare actual spending to your plan to spot problem areas quickly.

- What impulse purchases do I make? Tracking unplanned buys reveals patterns you can interrupt.

Answering these prompts helps you rethink habits and reclaim money you didn’t realize you were wasting.

How does finding spending leaks improve your budget?

Once you identify leaks, you can make deliberate changes that strengthen your budget. Knowing where your money goes lets you trim or reallocate spending to better match your goals. Typical leaks include:

- Frequent dining out: Cooking more at home can quickly add up to real savings.

- Unused subscriptions: Canceling unused services frees cash for higher priorities.

- Impulse buys: Slowing down purchases prevents budget drift.

Addressing these areas leads to steadier finances and more flexibility month to month.

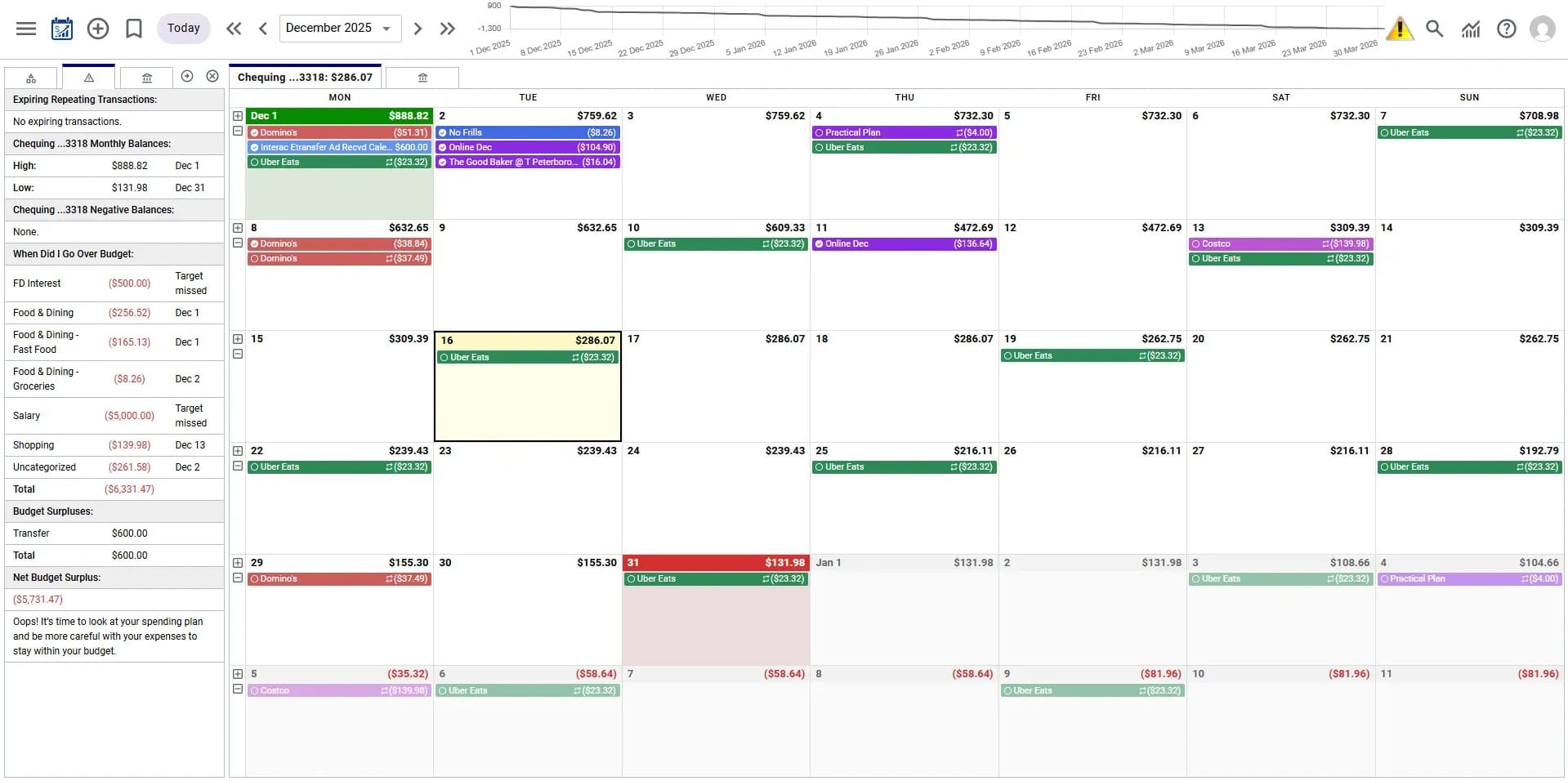

How can you use CalendarBudget to organize spending and save more?

CalendarBudget uses a calendar view to make income and expenses easy to see over time. That visual context helps you plan for bills, spot timing gaps, and set realistic goals. Add recurring items, schedule automatic savings, and watch progress toward your targets so you can adjust before problems build.

Practical tools like CalendarBudget make consistent budgeting and saving much easier—habits that research links to greater financial stability over time.

Budgeting & Saving for Personal Financial Stability

Effective personal financial management hinges on clear budgeting and consistent saving. A detailed budget helps you monitor cash flow, prioritize spending, and set short- and long-term goals. Studies show people who follow a budget regularly have stronger financial health and are less likely to fall into debt. Pairing budgeting with disciplined saving builds resilience and supports lasting financial progress.

Budgeting and saving effectiveness as the main pillar of sustainable personal financial management, T Prakoso, 2024

Which CalendarBudget features support solid financial planning?

CalendarBudget includes several practical features designed to make planning easier:

- Calendar-based interface: See money in time—when income arrives, when bills are due, and how spending clusters each month.

- Automated savings: Schedule transfers or set rules so savings happen without extra effort.

- Budget creation and tracking: Build budgets that reflect your priorities and monitor them in real time.

These tools help you make clearer decisions and keep your financial plan on track.

How does calendar-based budgeting clarify income and expenses?

Using a calendar turns abstract numbers into a timeline you can read at a glance. It highlights patterns—paychecks, bill spikes, and free periods—so you can plan for peaks and avoid surprises. Categorizing items on a calendar also shows where habits form, making it easier to course-correct.

What practical budgeting tips help adults 25–45 save more?

For people in their mid-20s to mid-40s, a few steady habits make a big difference. Try these:

- Start a rainy-day fund: Even a small emergency buffer prevents short-term shocks from turning into long-term problems.

- Track your expenses: Regular review helps you spot leaks and keep priorities in focus.

- Create a working monthly budget: A realistic, adjustable budget guides choices and keeps spending aligned with goals.

These steps build stability and create room to save for bigger goals.

Which budgeting strategies work well for monthly expense management?

Choose a strategy that fits your habits and goals. Common, effective approaches include:

- 50/30/20 rule: Split income into needs (50%), wants (30%), and savings (20%) for a straightforward framework.

- Zero-based budgeting: Assign every dollar a job so income minus expenses equals zero—great for tight control.

- Envelope system: Use separate buckets (or accounts) for specific categories to limit overspending.

Pick one and adapt it to your life; consistency matters more than perfection.

How can behavioral finance questions improve your money habits?

Behavioral finance questions force you to examine why you spend the way you do. Asking “What triggers my impulse purchases?” or “How do I feel after big buys?” reveals emotional and situational patterns. With that self-knowledge, you can design simple rules to avoid costly mistakes and steer toward healthier habits.

What should you ask before spending money?

Before you buy, run through a quick checklist:

- Do I really need this item? Separate wants from needs to prevent unnecessary purchases.

- How will this purchase affect my budget? Consider the short- and long-term impact on your plan.

- Is there a cheaper alternative? Comparison often uncovers better value and saves money.

These questions change impulse decisions into deliberate choices that align with your goals.

How do these questions help you prioritize needs over wants?

Asking clear questions creates distance between impulse and action. When you decide something is a want rather than a need, you give yourself permission to wait or look for a cheaper option. That pause is where smarter financial choices happen.

What role do these questions play in long-term planning?

Over time, habitually questioning purchases shapes where your money goes. Regularly checking choices against goals helps you adjust course early and keeps long-term priorities—retirement, emergency savings, major purchases—within reach.

How does asking the right questions lead to real savings?

Right-sized questions surface patterns and opportunities: recurring charges to cancel, categories to trim, or income to grow. Those insights let you design targeted strategies that produce measurable savings.

What are examples of smart questions that lead to savings?

Use these prompts to guide action:

- What are my financial goals? Clear goals make it easier to say “no” to distractions.

- How can I reduce monthly expenses? Identify concrete changes—subscriptions, dining, utilities—to lower costs.

- Am I making the most of my income? Look for side income, raises, or better returns on your money.

These questions shift you from passive spending to intentional money management, which grows savings over time.

How does reflecting on past spending give you more control?

Reviewing past decisions builds accountability and insight. When you track what you bought and why, you can spot habits to change and reinforce better choices. That ongoing reflection is the foundation of steady financial progress.

Leave A Comment