Plan To Use Your Tax Refund Wisely

For many households, a tax refund isn’t just a one‑off bonus — it’s a tactical chance to strengthen your finances and move faster toward long‑term goals. The difference comes down to intention: spend the money now, or use it to create lasting change. This guide walks through smart, practical ways to use your refund in 2026, helps you rank those options based on your situation, and shows how CalendarBudget lets you preview the impact of each choice before you move a dollar.

What Is a Tax Refund and Why Does It Matter in 2026?

At its simplest, a tax refund is money returned to you because you overpaid taxes during the year — often from payroll withholding or qualifying tax credits. In 2026, refunds matter more because policy changes, inflation, and broader economic shifts can affect how much you get and who qualifies for which credits. Knowing the factors that influence your refund helps you plan confidently instead of being surprised when the money arrives.

How Does Your Tax Refund Get Calculated?

Your refund starts with your total annual income. From that number, allowable deductions reduce your taxable income, and any tax credits you qualify for lower the tax you owe. Deductions — like mortgage interest, student loan interest, or pre‑tax retirement contributions — shrink the slice of income that’s taxed. Credits are even more powerful because they cut your tax bill dollar for dollar. Credits vary by country, but common examples include those for low‑income households, families with children, and education expenses. Understanding deductions and credits gives you a better estimate of what to expect and lets you plan how to use the refund.

What Impact Do Legislative Changes Have on Refunds?

Laws and tax rules change regularly, and those shifts can change refund amounts for some taxpayers. For example, the US Inflation Reduction Act of 2022 added several targeted credits — mainly for energy upgrades and certain clean‑energy purchases — that can affect refunds for eligible taxpayers. Not every law changes refunds for everyone, but adjustments to tax brackets, standard deductions, or specific credits can change year‑to‑year. Staying informed about rules in your region helps you maximize benefits and avoid surprises.

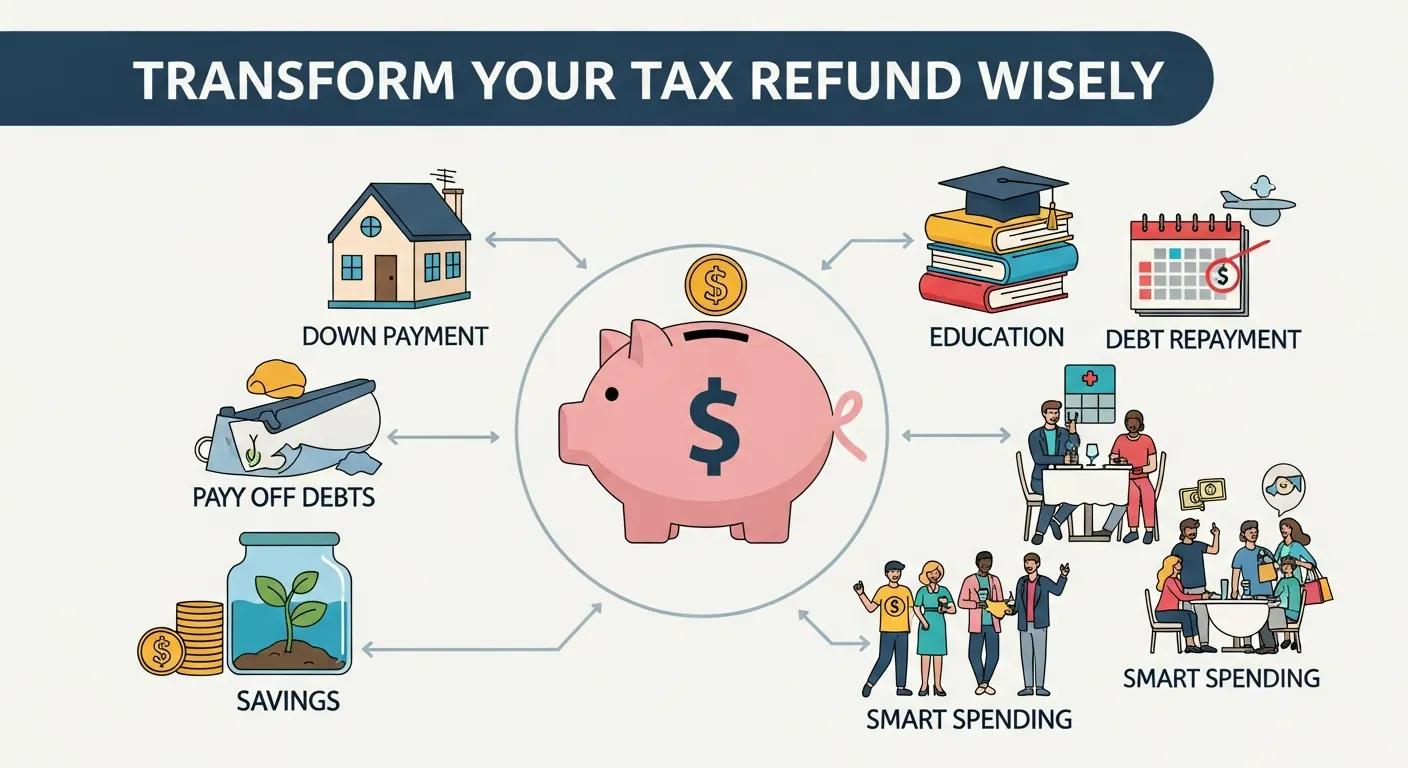

What Are the Best Ways to Spend Your Tax Refund?

When used intentionally, a refund can accelerate financial stability and progress. Below are common, high‑impact ways people allocate refunds — each carries a clear benefit depending on your priorities.

- Pay Off High-Interest Debt: Focus on credit cards, high‑rate personal loans, or similar debt first. Paying down these balances reduces the interest you’ll pay over time and frees up monthly cash flow. A one‑time refund payment can make a big, immediate dent — sometimes wiping out a balance entirely.

- Build or Boost an Emergency Fund: If you don’t have three to six months of essential expenses saved, adding to an emergency fund should be a priority. Even a partial contribution improves resilience against job loss, medical bills, or major repairs, and helps you avoid future high‑interest debt.

- Invest for the Future: With a solid emergency fund and manageable debt, use the refund to add to tax‑advantaged retirement accounts (IRAs, 401(k)s in the US, or local equivalents) or to education savings plans (like 529s in the US). These accounts help your money grow tax‑efficiently over time.

- Home Improvements that Add Value: Spend on repairs or upgrades that raise your home’s value or lower long‑term costs — for example, energy‑efficient improvements or essential maintenance that prevents bigger future expenses.

- Invest in Personal Development: Sometimes the best return is on yourself. Use a refund for a course, certification, or new skill that can boost your earning potential and career trajectory.

How Can Paying Off High-Interest Debt Improve Your Financial Health?

High‑interest debt — especially credit cards with APRs often in the double digits — can erode savings and slow progress. Using a refund to lower those balances saves money on future interest, reduces monthly minimums, and frees up cash for other goals. Lowering your credit utilization (the credit you’re using versus your total available credit) can also improve your credit score, making it easier to qualify for better loan rates later. Tackling high‑cost debt is one of the fastest ways to strengthen your financial footing.

Why Building an Emergency Fund with Your Refund Is Smart Money Management

An emergency fund is your financial shock absorber — money set aside so unexpected costs don’t spiral into debt. Experts typically recommend three to six months of basic living expenses. A single refund may not reach that target, but every contribution helps. Keep this fund in an easy‑access, separate account (ideally a high‑yield savings account) so it’s available when you need it, but not tempting for everyday spending.

How Can You Use Tax Refunds for Long-Term Financial Planning?

Beyond short‑term needs, a thoughtful refund allocation can accelerate long‑term goals. Aim your refund where it delivers the most durable value for your situation — retirement, education, or a home down payment, for example.

- Investing in Retirement Accounts: Adding money to tax‑advantaged retirement accounts (IRAs or 401(k)s in the US, or local equivalents) leverages tax benefits and compound growth. Traditional accounts may give you an immediate tax deduction; Roth‑style accounts offer tax‑free withdrawals later. Even modest refund contributions can grow substantially over decades.

- Contributing to an Education Savings Plan: Education plans like 529s (or regional equivalents) offer tax‑free growth and withdrawals for eligible education expenses. Some states or countries add incentives such as tax deductions or credits for contributions. Regular, even small, deposits from refunds can add up and reduce future tuition burdens.

- Saving for a Down Payment: A sizable refund can jump‑start or boost a down payment for a home. A larger down payment usually means lower monthly mortgage costs, less interest paid over the life of the loan, and a better chance of avoiding mortgage insurance.

What Are the Benefits of Investing in Retirement Accounts?

Tax‑advantaged retirement accounts provide two clear advantages: immediate tax benefits and long‑term growth. Contributions to traditional accounts often lower your taxable income today, while Roth‑style accounts grow tax‑free for qualified withdrawals in retirement. Combined with compound growth, these accounts can turn modest contributions into a significantly larger nest egg over time. Prioritizing retirement saving is a foundation of long‑term financial security.

How Does Contributing to an Education Savings Plan Support Family Financial Goals?

Education savings plans (like 529s in the US or similar programs elsewhere) are built to make paying for education easier. They typically offer tax‑free growth and tax‑free withdrawals for qualified education costs — tuition, fees, books, supplies, and sometimes room and board. In many places, there are additional incentives such as state tax deductions or credits for contributions. Steady contributions, including occasional boosts from refunds, help reduce future education costs and make planning for school more predictable.

How Does CalendarBudget Help You Manage and Visualize Your Tax Refund?

CalendarBudget is a personal finance tool focused on clear, visual planning. Instead of just showing today’s balance, CalendarBudget forecasts your expected bank balance day‑by‑day. That view makes it easy to see how a refund will affect upcoming bills, speed up savings goals, and change your cash flow over time.

How Does Visual Forecasting Empower Your Tax Refund Decisions?

Visual forecasting removes the guesswork. Enter an expected refund into your CalendarBudget forecast and you’ll immediately see the ripple effects: how much sooner a debt is paid off, how quickly your emergency fund grows, or how monthly cash flow changes after a large payment. That instant visual feedback lets you test different allocations — debt repayment, savings, investments, or a mix — and choose the plan that fits your goals.

What Features Assist in Allocating Your Refund to Debt, Savings, and Investments?

CalendarBudget gives you straightforward tools to put a refund to work. Set and track specific goals, see spending versus goals, and use the day‑by‑day forecast to assign refund dollars to exact categories — an extra credit‑card payment, a lump sum to savings, or a scheduled investment contribution. Watching the long‑term effects play out visually helps ensure your refund supports the outcomes you want most.

Leave A Comment