Provident Living Tools for Budgeting & Emergency Preparedness

Provident living is a practical, forward‑looking way to handle money that focuses on self‑reliance and clear planning. This piece breaks down those principles so you can strengthen your finances through steady budgeting, avoiding unnecessary debt, and being prepared for surprises. Many people feel stretched thin by bills and debt; adopting provident habits helps you regain control, grow savings, and be ready when life throws a curveball. It offers not just financial stability, but also a profound sense of peace and long-term security. Below we cover the essentials of preparedness, the role of straightforward budgeting, debt‑avoidance tactics, and how self‑reliance in daily life supports a truly prepared household.

What Is Provident Living — and Why Financial Preparedness Matters?

Provident living means living with a plan: saving for likely needs, protecting against risks, and aiming for greater self‑sufficiency. Financial preparedness matters because it creates a buffer when things go wrong — a job loss, a medical bill, or an unexpected repair. Being proactive lowers stress and gives you more choices when challenges arise. It transforms potential crises into manageable hurdles, allowing you to maintain stability and pursue opportunities even amidst economic shifts.

How Does Provident Living Promote Self-Reliance and Financial Security?

At its core, provident living builds practical skills you can use every day: budgeting, saving, and sensible investing. Those skills create a stable base you can rely on. This foundation empowers individuals to make independent financial decisions, reducing reliance on external aid and fostering a sense of control over their future. When you know where your money is going and why, you make better decisions and weather economic ups and downs with more confidence. People who practice these habits are often quicker to adapt during personal or market shocks.

What Are the Key Components of Financial Preparedness?

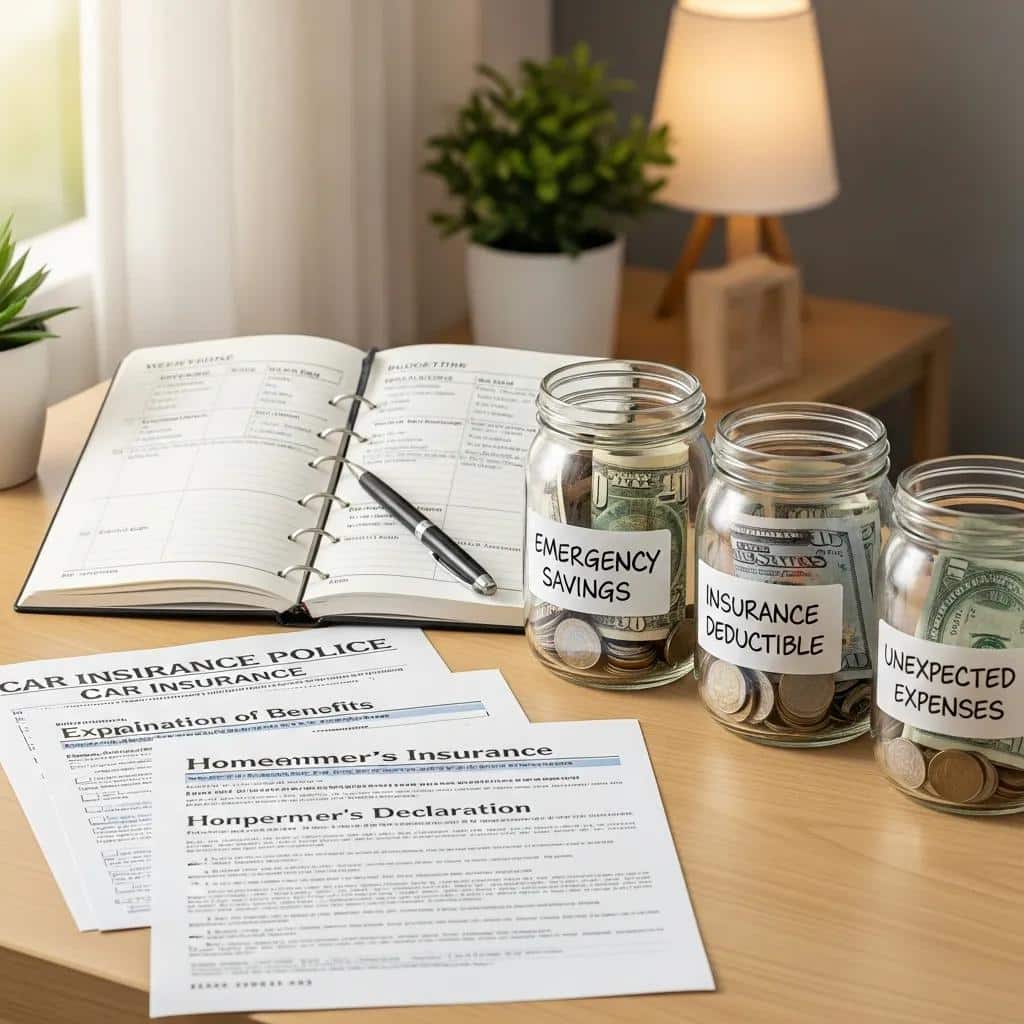

Financial preparedness combines a few simple, dependable pieces that work together. These include:

- Emergency Funds: A cash reserve for unexpected costs — think medical bills or car repairs — so you don’t have to borrow when something comes up. Aim for 3-6 months of essential living expenses. Start small, even $500, and build from there.

- Insurance: The right coverage protects you from big, draining expenses after life’s surprises. This includes health, auto, home/renters, and potentially life or disability insurance, tailored to your specific risks.

- Budgeting: A clear budget tracks income and expenses so you live within your means and keep saving toward goals. Explore methods like the 50/30/20 rule (50% needs, 30% wants, 20% savings/debt) or zero-based budgeting for optimal control.

Focus on these basics and you’ll have a practical plan that supports stability over time.

How Can Smart Budgeting Support Financial Security and Self-Reliance?

Smart budgeting turns intentions into action. It gives your money a purpose, helps you spot waste, and makes room for saving. With a good budget you can prioritize needs, set aside money for what matters, and build the habit of planning ahead.

What Is the CalendarBudget Method for Visual Cash Flow Forecasting?

The CalendarBudget method uses a visual day‑by‑day money planner to show future bank balances. Seeing your cash flow on a calendar makes it easier to plan for bills and avoid surprise shortfalls. It visually projects your bank balance day-by-day, highlighting future low points so you can adjust spending or payment timing proactively. When you can literally see what days are tight, you make smarter choices about timing payments and spending.

How to Manage Income and Expenses Effectively Using Visual Budgeting?

Use these steps to manage money with a visual budget:

- Track Income: Log every source of cash — paychecks, side work, or irregular payments — so you know what’s coming in. Utilize budgeting apps (e.g., CalendarBudget, YNAB), spreadsheets, or simple notebooks to capture every dollar.

- List Expenses: Split costs into fixed (rent, utilities) and variable (groceries, entertainment) to spot patterns and cut avoidable spending. Regularly review variable expenses for areas to cut, like subscriptions or dining out.

- Set Goals: Pick short‑ and long‑term targets — an emergency cushion, a trip, retirement — and schedule small, steady deposits toward them. Ensure goals are SMART: Specific, Measurable, Achievable, Relevant, and Time-bound.

Those steps help you build a budget that supports independence and realistic goals.

What Strategies Help Avoid Debt and Build Savings for Long-Term Stability?

Cutting unnecessary debt while growing savings is central to lasting financial health. The right tactics make debt repayment manageable and keep you from slipping back into risky credit use.

Which Debt Avoidance Techniques Foster Financial Independence?

Try these practical methods to reduce debt and strengthen control over your money:

- Debt Snowball Method: Pay off the smallest balances first while keeping minimums on larger debts — the wins keep you motivated. Consider the Debt Avalanche method as an alternative, which prioritizes debts with the highest interest rates to save more money overall.

- Budgeting for Debt Reduction: Carve out a steady portion of your income each month specifically for debt paydown so it stays a priority. Explore options like negotiating lower interest rates or debt consolidation for larger balances.

- Avoiding Unnecessary Purchases: Pause before buying — ask whether the purchase fits your priorities to cut impulse spending. Implement a ’24-hour rule’ for non-essential purchases: if you still want it after a day, then consider buying it.

Applied consistently, these practices help you shrink debt and free up cash for saving.

How to Set and Achieve Savings Goals for Emergencies and Retirement?

Make saving straightforward with a clear plan:

- Define Specific Goals: Name what you’re saving for — an emergency fund, a vacation, retirement — so your effort has direction. Make sure these goals are SMART (Specific, Measurable, Achievable, Relevant, Time-bound).

- Determine the Amount Needed: Estimate the target for each goal so you know when you’ll be finished. Research average costs for your goals to set realistic targets.

- Create a Savings Plan: Decide how much to save each month and schedule it automatically where possible to keep progress steady. Automate transfers to your savings accounts immediately after receiving income (‘pay yourself first’) to ensure consistent progress.

Small, consistent steps add up. Over time those savings become a solid financial foundation.

How Does Self-Reliance Extend Beyond Finances to Build a Prepared Household?

Self‑reliance isn’t just about money. Practical skills and routines around the house reduce costs and make your family more resilient when problems arise.

What Practical Skills Enhance Self-Reliance in Daily Life?

Here are everyday skills that boost independence and trim household costs:

- Gardening: Growing some of your own food cuts grocery bills and adds fresh produce to your table. Even a small herb garden can reduce grocery costs and provide fresh ingredients.

- Basic Home Repairs: Learning simple fixes saves on service calls and keeps small problems from becoming big ones. Learning to fix a leaky faucet, patch a wall, or reset a circuit breaker can save hundreds in service fees.

- Cooking: Cooking at home is usually cheaper and healthier than eating out, and it stretches your food budget further. Meal planning and batch cooking can further maximize savings and reduce food waste.

- Basic Sewing/Mending: Repairing clothes extends their life and reduces the need for new purchases, fostering resourcefulness.

These habits save money and build confidence in handling daily challenges.

How to Prepare Your Family for Emergencies and Financial Crises?

Preparation means having a plan and the resources to follow it. Consider these steps:

- Create an Emergency Plan: Outline roles and steps for events like natural disasters or sudden income loss so everyone knows what to do. Include evacuation routes, designated meeting points, and contact information for all family members and out-of-state contacts.

- Build an Emergency Fund: Aim for at least three to six months of basic living costs tucked away to cover unexpected shocks. This fund is your first line of defense against financial crises.

- Assemble an Emergency Kit: Stock non-perishable food, water (one gallon per person per day for at least three days), first-aid supplies, flashlights, batteries, a whistle, and important documents for at least 72 hours.

- Educate Family Members: Teach family members the plan and their responsibilities so the household can act quickly and calmly. Practice drills for fire or natural disasters, and ensure everyone knows where emergency supplies are stored.

Putting these measures in place increases your household’s resilience and peace of mind.

Quick Start Guide to Provident Living

Ready to take control of your finances and build a more resilient household? Here’s how to begin:

- Create a Simple Budget: Track your income and expenses for one month to understand where your money goes. Use an app, spreadsheet, or notebook.

- Start an Emergency Fund: Aim for an initial $500-$1,000. Automate small, regular transfers to a separate savings account.

- Tackle High-Interest Debt: Prioritize paying down credit cards or personal loans using the snowball or avalanche method.

- Learn a Practical Skill: Pick one skill like basic cooking, mending, or simple home repairs to reduce expenses and boost confidence.

- Review Your Insurance: Ensure you have adequate coverage for health, auto, and home to protect against major financial setbacks.

Adopting provident living practices — steady budgeting, deliberate debt reduction, and useful life skills — makes your finances more secure and your household more capable. These habits give you options, lower stress, and help you face uncertainty with a clear plan instead of worry, ultimately leading to a more fulfilling and resilient life.

Leave A Comment